Calibrate Review: The Insurance-First GLP-1 Program (May 2026)

You have commercial insurance. You have a BMI over 30. Your doctor mentioned Wegovy or Zepbound. Then you opened an Explanation of Benefits and discovered the prior-authorisation process — a bureaucratic obstacle course where insurers routinely deny first requests, demand peer-to-peer reviews, and lose paperwork.

Calibrate was built for exactly that frustration. The company’s entire value proposition is: we will fight your insurance company so you don’t have to, then put you through a year-long coaching programme so the weight doesn’t come straight back.

That proposition has worked well for many of its members. It has also failed badly for a meaningful subset. Understanding which camp you’re likely to land in is what this review is for.

At a Glance

| Feature | Calibrate |

|---|---|

| Programme type | 12-month structured Metabolic Reset |

| Membership fee | $199/month (3-month minimum) |

| Medication | Branded GLP-1s only via your pharmacy |

| Compounded drugs | No |

| Insurance required | Yes — commercial only (ages 18–64) |

| Drug copay (est.) | $25/month or less after deductible |

| Prior-auth handled by | Calibrate’s insurance team |

| Coaching | Biweekly 15-min video sessions |

| Money-back guarantee | 50% refund if <10% weight loss at 12 months |

| Not available to | Medicare / Medicaid / Tricare / >age 64 |

What Calibrate Actually Is

Calibrate is not a prescription service with light coaching bolted on. It is a year-long metabolic programme where the prescription is the entry point, not the product. The company calls this a “Metabolic Reset,” and the framing matters: Calibrate’s argument is that GLP-1 drugs alone are not sufficient for durable weight loss, and that the lifestyle curriculum is what converts drug-assisted weight loss into a reset metabolic set point.

Whether that argument holds up is scientifically contested — most obesity-medicine researchers accept that most people regain significant weight after stopping GLP-1s, regardless of behavioural coaching. Calibrate’s own published data show 16% average weight loss at 12 months and 19% at 36 months across its member cohort, which is consistent with the clinical-trial literature for GLP-1s. The attribution question — how much is the drug and how much is the coaching — remains open.

What distinguishes Calibrate structurally from every cash-pay or compounding competitor is this: Calibrate does not dispense medication. It prescribes branded FDA-approved GLP-1s through a clinical team and sends those prescriptions to your insurance pharmacy. You pay your insurance copay. Calibrate collects its membership fee separately.

This structure has a specific implication: if your insurance denies the prior authorisation, Calibrate cannot fall back on a compounded or cash-pay option. There is no plan B inside the programme.

Pricing: What You Actually Pay

The headline is $199/month, but the real cost requires two numbers.

Membership fee: $199/month, billed monthly with a 3-month minimum. That is $597 committed upfront before you have received a single GLP-1 dose. After the initial 3 months, it renews monthly until you cancel. The membership is HSA/FSA eligible; it is not reimbursable by insurance.

Drug cost: This is separate and billed through your insurance at your pharmacy. Calibrate states that most members with commercial insurance pay $25/month or less after the deductible is met. That figure is real — commercial insurance with a weight-loss benefit routinely brings GLP-1 copays to $25 or below once PA is approved. But two caveats apply: first, you must meet your annual deductible before copay rates kick in; second, approximately 20% of Calibrate members ultimately do not get insurance coverage approved. Those members either pay the full cash price for the branded drug (currently $1,400+ per month without a manufacturer coupon) or exit the programme with a refund.

Annual cost range:

- Best case (insured, deductible met): ~$2,688 ($199×12 + $25×12)

- Median case (deductible not yet met for part of year): $2,988–$3,500

- Worst case (PA denied, refund requested): $597 paid for the 3-month minimum, minus $250 processing fee if refund is issued

Calibrate also offers Affirm financing at 0% APR, which spreads the membership cost but does not change the total.

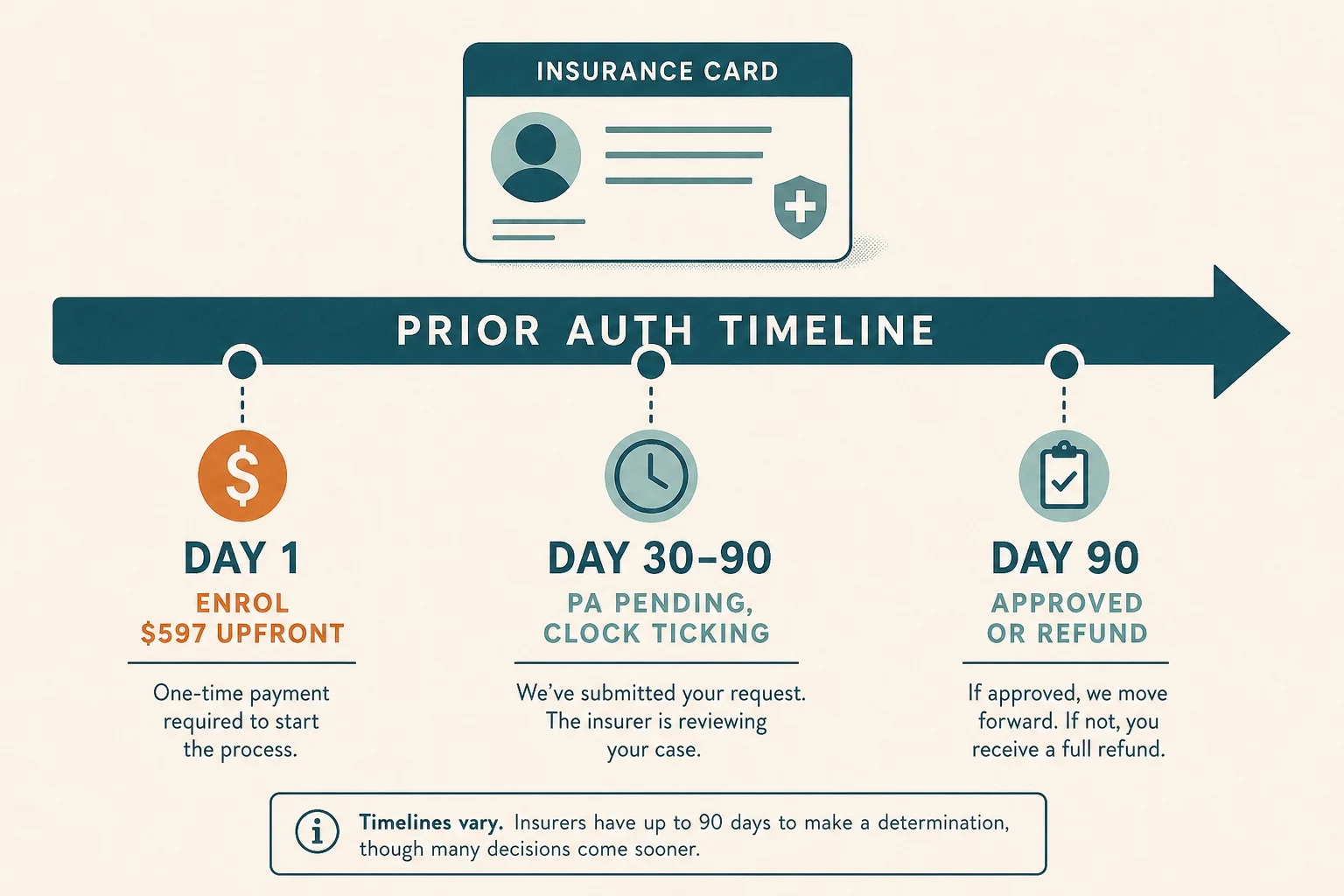

The Prior-Auth Process: How Calibrate Handles It

This is Calibrate’s most advertised capability, and the one most responsible for both its best and worst reviews.

When you enrol, Calibrate’s insurance team takes over the prior-authorisation process on your behalf. They submit the clinical documentation to your insurer, manage appeals if the first request is denied, and coordinate peer-to-peer reviews between Calibrate clinicians and insurance medical directors. The goal is to land you at a $25 monthly copay with a 12-month approval.

The process typically takes 6–8 weeks. The Calibrate website acknowledges a 90-day window, and the company guarantees a refund (minus a $250 administrative fee) if it cannot secure approval within 90 days.

The practical problem: you are paying $199/month from day one, regardless of whether the prior auth has cleared. Members who waited 10–12 weeks for approval paid $398–$597 in membership fees before touching a single dose of medication. Members in the Business Insider 2023 investigation described waits of up to six months and communication that amounted to generic status messages with no actionable detail.

This is a known structural tension in the Calibrate model. The company acknowledges it: you are paying for the programme infrastructure — coaching setup, clinical onboarding, curriculum access — not just for the prescription itself. Whether that framing feels fair depends heavily on whether your insurance ultimately approves.

For patients who want to understand the full prior-auth landscape before committing, our guide to GLP-1 prior authorisation appeals covers the criteria most commercial insurers use, and what to do if a first request is denied.

The 12-Month Programme Structure

Calibrate’s “Metabolic Reset” is structured around four sequential phases. Each phase has a defined focus, and the curriculum is delivered through weekly lessons in the Calibrate app covering four pillars: food, sleep, exercise, and emotional health.

Months 1–3 (Learning). You receive your GLP-1 prescription, begin filling through insurance, and start biweekly 15-minute video coaching sessions. Weekly lessons establish the four pillars. Most members see measurable weight change within this phase, which is the highest-engagement period.

Months 3–6 (Practicing). The curriculum shifts from principle to application. Modular focus classes become available for issues specific to each member. Biweekly coaching continues. The pace of lessons increases to approximately two per week.

Months 6–9 (Setting and Reinforcing). The emphasis moves to habit consolidation. Calibrate introduces journaling and mindset work to reinforce behavioural change at the identity level rather than the rule level.

Month 9 onwards (Sustaining). Biweekly check-ins focus on maintenance and selection of additional focus classes. This phase extends as long as the membership continues.

Each clinical visit is a 30-minute video appointment with a board-certified clinician; the cadence of these visits depends on where you are in the dose-titration schedule. Labs are ordered at baseline and reviewed at clinical visits, covered by your insurance.

The drug list available through Calibrate as of May 2026: Wegovy (semaglutide), Zepbound (tirzepatide), Ozempic (semaglutide, off-label for weight), Mounjaro (tirzepatide, off-label), and Foundayo (dulaglutide). Prescriber determines which drug is appropriate; the decision follows clinical guidelines and what your insurance plan covers.

Sign-Up and Intake Experience

Calibrate’s intake is more thorough than most GLP-1 telehealth platforms. The sequence:

-

Eligibility check. You confirm commercial insurance, age 18–64, and BMI ≥30 (or ≥27 with at least one qualifying metabolic condition: pre-diabetes, hypertension, dyslipidaemia, cardiovascular disease, sleep apnoea, NAFLD, or PCOS).

-

Insurance verification. Calibrate confirms your plan has a weight-loss benefit before you enrol. This step filters out patients whose insurance will definitively not cover GLP-1s.

-

First coaching session. Before you see a clinician, you meet your coach and set programme goals. This session sets the tone for the coaching relationship.

-

Lab draw. A full metabolic panel is ordered through insurance at Quest Diagnostics or a comparable lab. Results inform the first clinical visit.

-

Clinician video appointment. A 30-minute visit with a board-certified physician reviews your labs, history, and drug options. The prescription is written here.

-

Prior-auth submission. Calibrate submits to your insurer. The wait begins.

-

Welcome kit. A smart scale ships during the intake period and connects to the Calibrate app for weight tracking.

From application to first dose: typically 8–12 weeks, with the insurance-approval window as the primary variable.

Support Quality: What Members Actually Say

Calibrate’s coaching gets the strongest reviews. On Trustpilot (4.6/5 across 1,219 reviews as of May 2026), the most consistent praise is for coaches who are described as “genuinely invested,” “non-judgemental,” and “the reason I stayed.” The curriculum draws specific compliments from members who valued the emotional health and sleep modules, which are thin-to-nonexistent at most GLP-1 telehealth competitors.

The customer service layer — the piece that sits between a member and their insurance situation — is a different story.

A 2023 Business Insider investigation, based on interviews with 19 current and former Calibrate employees and review of hundreds of verified member complaints, documented the following pattern: the prior-auth team was frequently understaffed relative to enrolment; response times in the member app reached 10 calendar days at peak disruption; members experiencing insurance problems received generic replies from staff who had no real-time view into prescription status; and two rounds of layoffs in 2022–2023 reduced the engineering team responsible for the app to a “skeleton crew.”

At its worst, a member described to Business Insider how she waited six months for an initial approval, lost 50 pounds, then hit an expiring insurance approval and went another two weeks without a response — before giving up and switching providers entirely.

Calibrate’s BBB profile carries over 700 complaints filed in the past 12 months. The BBB issued a marketplace alert citing a “marked increase” in reports involving medication delays, unresponsive customer service, and difficulty securing refunds or ending payment plans. Calibrate is not BBB-accredited. Its BBB customer rating stands at 1.01/5 from 93 reviews.

The real picture sits somewhere between the Trustpilot and BBB distributions. Members who cleared prior auth smoothly and had a good insurance situation tend to have strong programme experiences. Members who hit insurance problems, app issues, or needed to cancel are disproportionately represented in the complaint record.

Cancellation: The Known Friction Points

Calibrate requires a 3-month minimum commitment. That is disclosed up front and is contractually enforceable. The issues arise in two other areas.

Post-commitment cancellation difficulty. Multiple BBB complaints describe members who attempted to cancel after the 3-month window and continued to be billed for months. The documented pattern: in-app-only support channel, slow responses, no direct phone line, and billing continuing through the response cycle. One complainant described being billed for over a year after initiating cancellation.

Refund denials at the 90-day drug-access guarantee. Calibrate guarantees a refund (minus $250) if it cannot secure drug access within 90 days of the first clinical appointment. Members who hit that deadline report being denied refunds on the grounds that they did not sufficiently engage with the programme — for instance, by not completing a required percentage of curriculum check-ins. This catch has surprised members who believed the guarantee to be unconditional.

The 10% weight-loss guarantee. The 50% membership refund after 12 months of <10% weight loss also carries conditions: members must have completed the coaching and curriculum requirements. Members who paid for a year and found the drug access gaps left them effectively outside the programme have run into difficulty qualifying.

Before enrolling, read Calibrate’s full terms at joincalibrate.com. The guarantee language contains specific programme-completion conditions.

Best For / Not For

Best for:

- Adults 18–64 with commercial insurance that covers weight management

- Patients whose insurer has a history of approving GLP-1s with structured programme requirements

- Members who actively want the coaching, curriculum, and accountability structure — not just the prescription

- Patients who can tolerate a 6–12 week wait for drug access and have the financial cushion to pay membership during that window

- Employees whose employer covers or subsidises Calibrate through an enterprise partnership (FedEx/OptumRx is the documented example)

Not for:

- Anyone on Medicare, Medicaid, Tricare, or without commercial insurance

- Adults over 64

- Adults with Type 1 or Type 2 diabetes (explicitly excluded from Calibrate eligibility)

- Anyone planning a pregnancy within 2 years or with active cancer or eating disorder history

- Patients who need medication within 1–2 weeks

- Anyone who wants a cash-pay or compounded fallback if insurance denies

- Patients whose primary goal is the cheapest possible access to a GLP-1

Calibrate vs Mochi vs PlushCare

| Feature | Calibrate | Mochi Health | PlushCare |

|---|---|---|---|

| Membership fee | $199/mo (3-mo min) | $79/mo | $19.99/mo |

| Drug model | Brand-name via your insurance pharmacy | Brand-name (insured) or compounded (cash-pay) | Brand-name via your insurance pharmacy |

| Compounded option | No | Yes (§503A) | No |

| Insurance required | Yes (commercial only) | No (cash-pay available) | No (brand-name cash copay available) |

| PA navigation | Full managed service | Active support | Care team handles PA |

| Coaching depth | Biweekly video + 12-month curriculum | Monthly video + dietitian | Scheduled video visits, follow-up at wk 2/4/8 |

| Age limit | 18–64 only | 18+ | 18+ |

| Time to first dose (est.) | 6–12 weeks (PA dependent) | 1–3 weeks (varies) | 1–4 weeks (PA dependent) |

| T2 diabetes eligible | No | Yes (discuss with prescriber) | Yes |

| Active litigation risk | None material | Eli Lilly lawsuit active (Apr 2026) | None material |

| Outcome data published | Yes (19% at 36 mo) | Limited | Not published |

For a side-by-side view across more providers, see our full provider comparison. For Mochi’s full profile, see the Mochi Health review. For PlushCare’s full profile, see the PlushCare review.

The Bottom Line

Calibrate’s insurance-first model is coherent. It solves a real problem — prior authorisation is genuinely hard for patients to navigate alone — and it wraps that solution in a structured programme with coaching that consistently draws strong reviews.

The material risk is timing and contingency. The prior-auth clock runs on Calibrate’s schedule, not the insurance company’s. You pay $199/month regardless. If your insurer denies the claim and the appeals exhaust the 90-day window, you can get a partial refund — minus a $250 fee — but you cannot switch to a compounded fallback inside the programme. The customer service layer that manages these contingencies has generated more complaints than Calibrate’s coaching layer, which is where the real operational risk lives.

If you have commercial insurance, are aged 18–64, can wait 6–12 weeks for medication, and are genuinely interested in the coaching — not just the prescription — Calibrate is a serious programme with published outcomes data to back it up. If any of those conditions do not apply, review your options at our provider comparison page or look at how to minimise out-of-pocket costs at cheapest places to get Wegovy.

Frequently Asked Questions

How much does Calibrate cost per month in 2026?

Calibrate’s Metabolic Reset membership costs $199/month as of May 2026, with a 3-month minimum commitment ($597 upfront). After the initial 3 months, membership renews monthly and can be cancelled. The membership fee is not insurance-covered but is HSA/FSA eligible. Medication fills separately through your insurance at your pharmacy — most members with commercial insurance pay $25/month or less after the deductible.

Does Calibrate accept Medicare or Medicaid?

No. Calibrate requires commercial insurance. Medicare, Medicaid, Tricare, and other government-payer plans are not eligible. Members must be aged 18–64.

How long does Calibrate’s prior authorisation take?

Calibrate states a 90-day window to secure insurance approval; the company guarantees a refund (minus a $250 processing fee) if it cannot get approval within that period. In practice, members have reported waits of 6 to 12 weeks. During that time, the $199/month membership fee continues.

Does Calibrate use compounded GLP-1s?

No. Calibrate prescribes FDA-approved branded GLP-1s only — Wegovy, Zepbound, Ozempic, Mounjaro, and Foundayo. Calibrate does not dispense medications or use a partner pharmacy; prescriptions are filled at the member’s own insurance pharmacy.

Can I cancel Calibrate after the first month?

No. Calibrate requires a 3-month minimum commitment. After the initial 3 months, you can cancel monthly. Members who have tried to cancel during the commitment period report significant friction — including slow responses and continued billing. BBB complaint records document cases of members being billed for months after attempting to cancel.

What is Calibrate’s 10% guarantee?

Members who complete 12 consecutive months of the programme and do not lose at least 10% of their starting body weight are eligible for a 50% refund on membership fees. The guarantee has conditions — members must complete the required coaching sessions and curriculum. The full refund policy is in Calibrate’s terms at joincalibrate.com.

Is Calibrate available in all 50 states?

Calibrate is available nationwide but accepts only commercial insurance for members aged 18–64. Adults over 65 and those on government-payer plans cannot enrol.

How does Calibrate compare to Mochi Health?

Calibrate is insurance-primary, brand-name-only, and programme-heavy — best suited to insured patients who want structured coaching and are not in a hurry. Mochi Health offers both insurance navigation and a compounded cash-pay option, with faster onboarding but an active Eli Lilly lawsuit against its compounding programme. Calibrate’s outcomes data (19% weight loss at 36 months) is more robust than most published telehealth comparisons, but requires full programme commitment to qualify.